Recommended citation format: Schnitkey, G., B. Sherrick, N. Paulson, C. Zulauf, J. Coppess and J. Baltz. "Premium Support and Crop Insurance: An Analysis of the Proposed 4% Farmer-Premium Payment Cap." farmdoc daily ( 13 ): 117, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, June 27, 2023. Permalink

Subsidies for crop insurance are being debated as the farm bill begins to come into focus. Subsides related to premium support for farmers have raised concerns in the past. Recent proposals have suggested an increase in premium support targeted at higher-risk farmland. Herein we provide background on premium support and an analysis of the impacts of a recently proposed 4% cap on farmer-paid premiums as a share of liability. The design of crop insurance already provides higher per-acre support to higher-risk areas and providing more support is highly questionable from a policy perspective.

Crop insurance is a Federally subsidized program. Many farmers would not buy crop insurance without subsidies, particularly in lower-risk areas like the Midwest. By providing subsidies, more farmers use crop insurance as a risk management tool. Encouraging widespread use of crop insurance is seen as a way to move away from ad hoc disaster assistance programs, which have undesirable characteristics. Ad hoc disaster assistance is never known until Congress enacts it, hence the name ad hoc. It thus cannot be built into risk management plans, reducing their benefits to farmers and lenders. Crop insurance use has become widespread, and ad hoc disaster spending was relatively low from 2002 to 2017, averaging $2.3 billion per year compared with over $11 billion per year (both in real $2023) from 1998 to 2001. In recent years, however, ad hoc programs have re-emerged in the form of the Wildfire and Hurricane Program (WHIP), WHIP+, and Economic Recovery Program (ERP) (see farmdoc Daily, June 6, 2022, June 7,2022, and June 14, 2022). Payments from the Market Facilitation and Pandemic Assistance programs since 2018 also represent significant levels of support through disaster assistance designs.

The Risk Management Agency (RMA) administers the Federal crop insurance program and sets its premiums. When setting “total” premiums, RMA is instructed in legislations to develop premiums such that the U.S. program is actuarially sound, meaning that total premiums should equal crop insurance payments over time. Over time, loss ratios from Federal crop insurance — insurance payments divided by total premium — should average 1.0, or slightly below. The 1.0 target differs from commercial, non-subsidized products, where loss ratios between .50 and .67 are more typical. Lower target loss ratios are needed to provide for loss reserves when payments are larger than normal, to cover administrative costs, and to generate profit for the risk bearing involved.

Federal support for Federal crop insurance comes in three primary forms:

By a large margin, premium support is the largest Federal outlay associated with crop insurance. During farm bill discussions, a common suggestion is to limit premium support to provide funds for other priorities. For example, a recent Governmental Accounting Office report suggests limiting the total amount of premium support to a farming operation (GAO-23-106228). During previous farm bills, similar discussions have occurred.

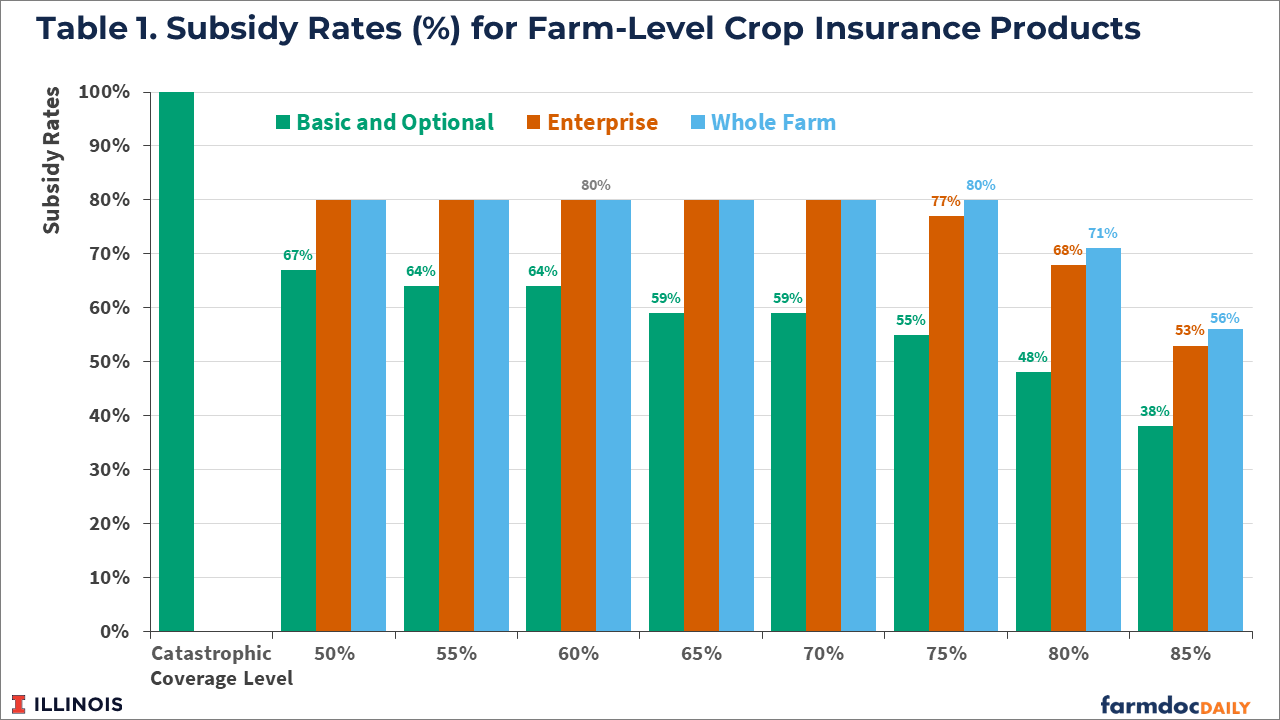

Premium support is calculated using subsidy rates set by Congressional action. These subsidy rates are permanent in the sense that they will stay the same until Congress again changes the statutory rates. Subsidy rates vary by coverage level and by unit, as is illustrated in Table 1, which shows rates for products that insure farm-level yields and revenue. Subsidy rates decrease with higher coverage levels, meaning that farmers pay more of the premium at higher coverage levels. For basic and optional units, subsidy rates are 100% at a Catastrophic (CAT) level, meaning that farmers do not pay premiums (there are administrative fees). CAT coverage is at a 50% coverage level with lower possible payments than at a 50% level. Subsidy rates decline to 38% at an 85% coverage level.

Subsidy rates vary by unit:

The current basic and optional unit subsidy rates were set in the Agricultural Risk Protection Act of 200. ARPA increased subsidies, lowering the out-of-pocket costs for the farmer which resulted in higher participation in crop insurance. Higher subsidies for enterprise and whole farm units were instituted in the 2008 Farm Bill, aiming to encourage enterprise unit use as ways to manage risk across the crop at a lower cost to the producer. Enterprise units also reduce the record-keeping and validation concerns with optional and basic units. The use of enterprise units increased after the 2008 Farm Bill was implemented.

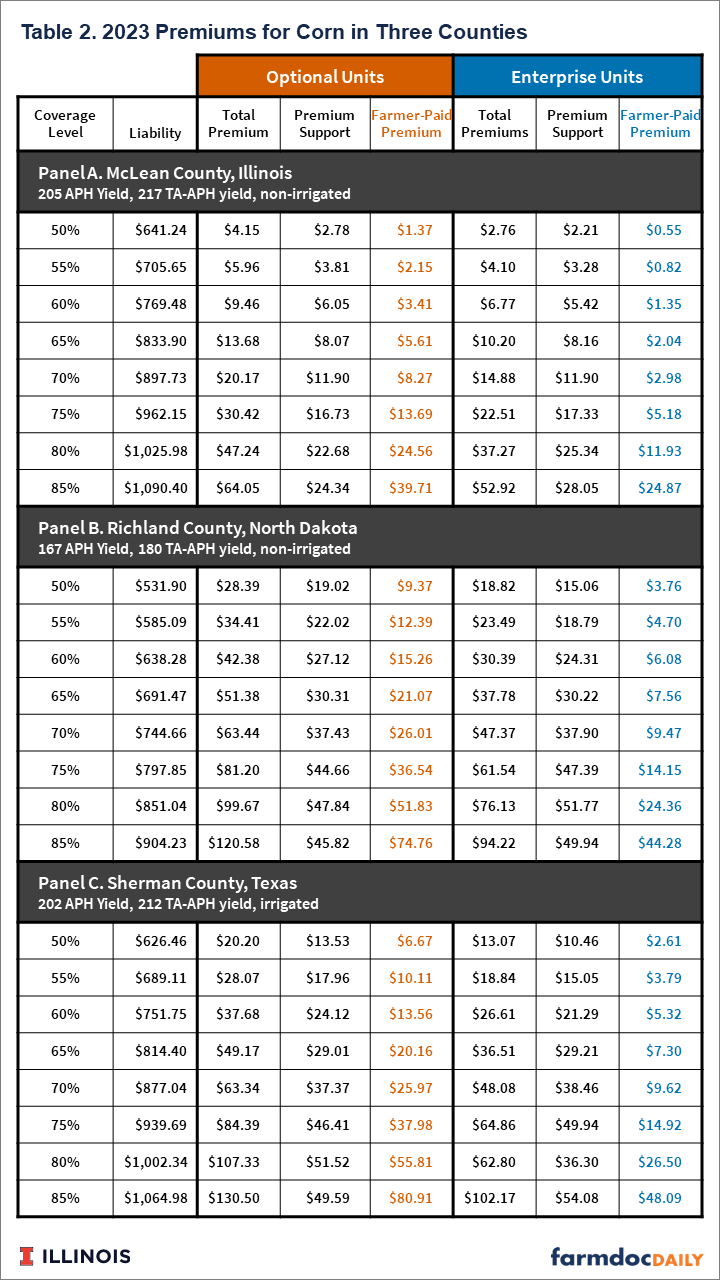

Table 2 shows 2023 premiums for corn in three counties in different states, thereby illustrating the impact of subsidies. Premiums are shown for Revenue Protection (RP), the most used product. Premiums are given for optional and enterprise units. Basic unit premiums will be between optional and enterprise units. Each county is a large production county in their respective states. The counties are:

The first column of Table 2 shows the liability for each product. Liability represents a measure of potential losses from a product. In Table 2, liability equals trend-adjusted Actual Production History (APH) yield times projected price times coverage level. Liability is directly related to expected production. Given the same guaranteed yields, liability would not vary across units.

Total premiums are the lowest for McLean County, the lowest yield risk county of the three. For an optional unit, the total premium at the 85% coverage level is $64.05 per acre. Total premiums in the $60 level are reached by the 70% coverage levels in Richland County, North Dakota ($63.44 per acre) and Sherman County, Texas ($63.34 per acre). The higher premiums in these two countries reflect the increased riskiness of production in these counties and thus the increased likelihood of insurance indemnity payments.

Because total premiums are lower, premium support on a dollar/acre basis is also lower for McLean County, Illinois. At an optional unit level, premium support ranges from $2.78 per acre at the 50% coverage level to $24.34 at the 85% coverage level for McLean County. Premium support on a dollar /acre basis is much higher in both North Dakota and Texas. At a 75% coverage level, premium support is $46.41 in Sherman County, 2.77 times higher than the $16.73 in McLean County, Illinois. At a 75% coverage level, similarly, Richland County, ND premium support is $44.61 per acre, or 2.77 times higher than the $16.73 in McLean County, Illinois. Because of the different risks of production in the respective counties, farmers purchasing the same coverage level (75%) receive far more in federal premium support in Richland County, ND and Sherman County, TX.

To summarize, the relationship between the various insurance variables goes as follows:

Higher premium subsidies can encourage the production of higher-risk crops in higher-risk areas. During the past twenty years, corn and soybean production has grown in Richland County, North Dakota, while corn and cotton production has grown in Sherman County, Texas. Many factors have influenced this growth, including the introduction of ethanol and continued growth in soybean exports. Higher subsidies to crop insurance did not hinder this growth.

Recently, Bullock and Steinbach introduced the idea of a 4% cap on farmer-paid premiums as a percent of liability (farmdoc Daily, June 5, 2023). Under this proposal, the total premium would stay the same, and premium support would increase to cover a larger share of the total premium, reducing farmer-paid premiums in areas of higher risk, particularly at higher coverage levels.

The cost of this proposal was estimated at $186 million based on an analysis of enterprise units for Actual Production History (APH), Revenue Protection (RP), RP with harvest price exclusion (RPHPE), and Yield Protection (RP) products, using data contained in the Summary of Business for 2022 (farmdoc Daily, June 5, 2023). If this proposal is introduced in farm bill discussion, an offset would need to be found in some other farm bill program. Moreover, the $186 million could underestimate the Federal outlays of the program for three reasons:

We provide an analysis of regions using the above three case farms, and then discuss within county impacts

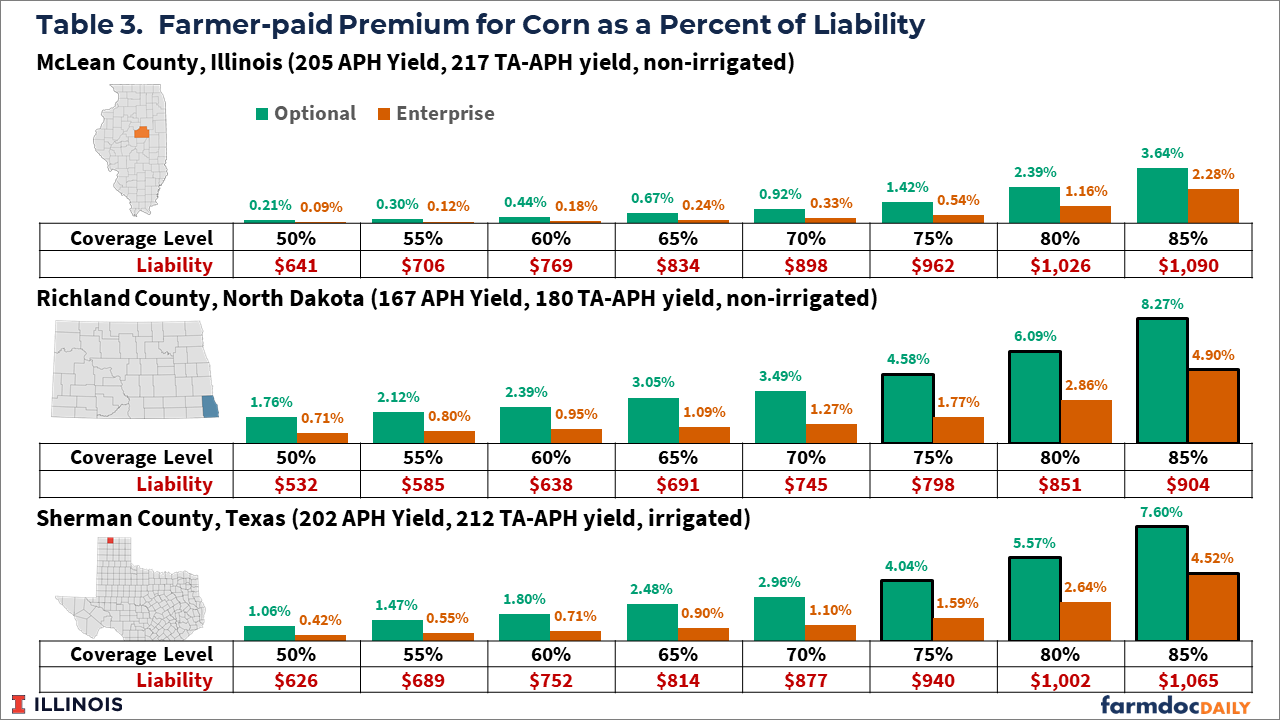

To illustrate regional impacts, Table 3 shows farmer-paid premiums as a percent of liability for the three counties in Table 2. In McLean County, Illinois, farmer-paid premium does not exceed 4%. The highest level is 3.64% for optional units at the 85% coverage level. Thus, the proposed 4% cap would not impact the average policy in McLean County, Illinois.

A 4% cap, however, would have an impact at the enterprise unit level on both Richland County, North Dakota and Sherman County, Texas. The 85% farmer-paid premium in Richland County would be reduced to $36.91, down by $12.75 from $44.66. To remain actuarially fair, the Federal premium subsidy would need to increase by a corresponding dollar amount. Thus, the $12.75 decrease at the 85% level would increase premium support by $12.75 per acre. In Sherman County, the 85% enterprise unit level would be reduced to $42.59, a reduction of $1.68 from $44.28.

If it were allowed, a 4% cap would have a much larger impact on optional unit premium. For optional units in Richland County, North Dakota, farmer-paid premiums exceed 4% at 75% and higher coverage levels. If adopted, the 4% premium rate cap would result in farmer-paid premium for optional units by coverage level as shown below:

When the cap is exceeded for both optimal and enterprise units, the farmer-paid premiums for enterprise and optional units would be the same. In the Richland County case, enterprise and optional units would both have a $36.17 farmer-paid premium. When faced with this situation, farmers would likely switch from enterprise to optional units, as there is a higher chance of payment with optional units.

There is the potential for some policies to exceed the 4% threshold even in counties with average farmer-paid premium as a percent of liability below 4%. These policies will have higher risks. Some of those polices will have substitute t-yields for actual yields in their guarantee. “High risk” farmland also will have the potential to have farmer paid premiums above 4% of liability.

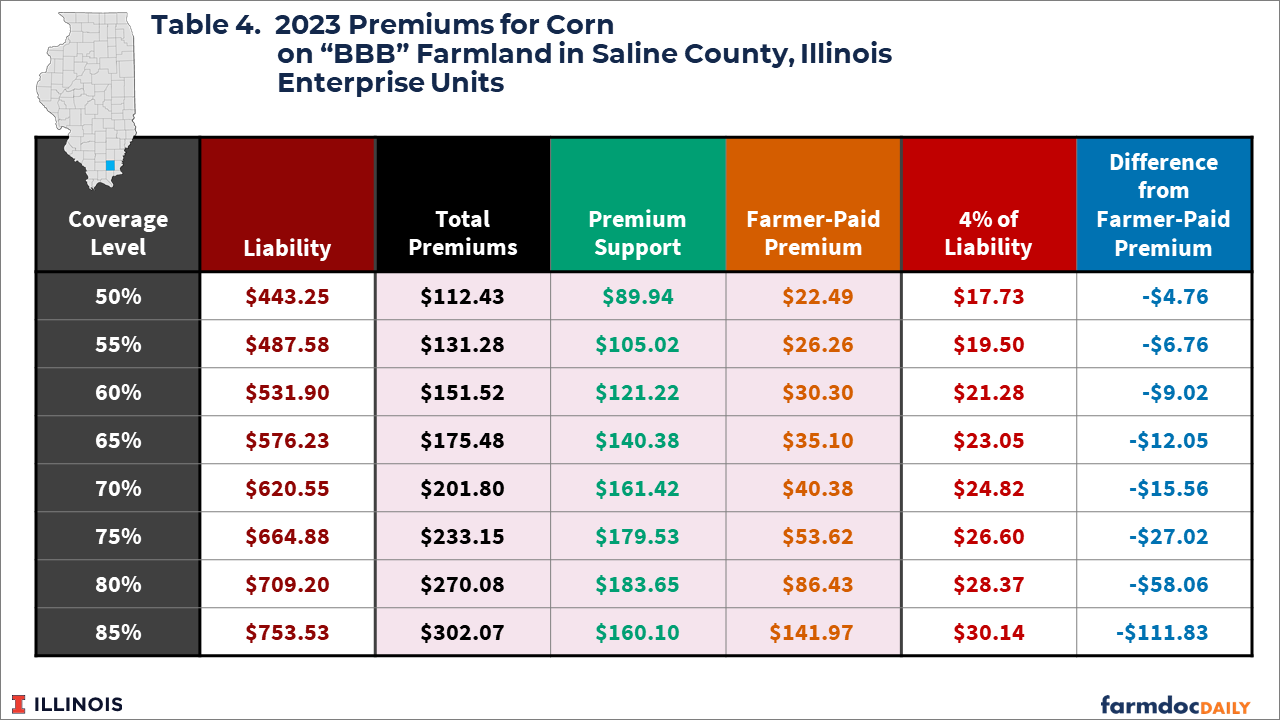

“High-risk” farmland often is prone to flood, and often have prevent plant claims. Premiums for high-risk land are much higher, reflecting the increased likelihood of claim, and this proposal would lower those premiums. Table 4 provides an example of high-risk premiums in Saline County, Illinois. This “BBB” farmland is a class of high-risk farmland. Farmer-paid premiums of over $302.07 per acre at an 85% coverage level. A 4% cap would cause the farmer-paid premium to decline by $111.83 per acre to $30.14 per acre. The reduced 85% premium is near the current $22.49 premium for the 50% coverage level. Farmers would increase their coverage levels, increasing the costs to the taxpayer, and increasing the risks born by crop insurance companies and the Federal government.

As currently designed, premium support provides higher per-acre subsidy amounts to higher-risk areas. A 4% cap on farmer-paid premiums would further increase, in some cases dramatically increase, support for higher-risk areas.

The incentive to produce more in higher risk area would increase. Is this good policy? Is this good expenditure of taxpayer dollars? Why should farmers in high-risk areas receive more premium support than farmers in lower-risk areas? Within an area, why would high risk farmland receive more premium support than lower risk area. Premium support has raised public-policy concerns in the past. Desirability of providing more support for higher-risk areas and farmland is questionable.

U.S. Government Accountability Office. (2023). Farm Bill: Reducing Crop Insurance Costs Could Fund Other Priorities (Report No. GAO-23-106228). Retrieved from https://www.gao.gov/products/gao-23-106228.

Zulauf, C., G. Schnitkey, J. Coppess, and N. Paulson. "The Importance of Insurance Unit in Crop Insurance Policy Debates." farmdoc daily (13):107, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, June 12, 2023.

Bullock, D., S. Steinbach. "Economic Consequences of Capping Premiums in Crop Insurance." farmdoc daily (13):102, Department of Agribusiness and Applied Economics, North Dakota State University, June 5, 2023.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.